Suppose the long-run cost function is C = 2q2. What is the cost-output elasticity for this case?

A) 1

B) 2

C) 1/2

D) 4

B

You might also like to view...

Suppose all firms in a perfectly competitive industry have production processes characterized by the production function  . Suppose the cost of labor is 20 and the cost of capital is 10.

a. Suppose that the industry is in long run equilibrium and that firms are using 1 unit of capital. What is the short run cost function of each firm?

. Suppose the cost of labor is 20 and the cost of capital is 10.

a. Suppose that the industry is in long run equilibrium and that firms are using 1 unit of capital. What is the short run cost function of each firm?

b. Suppose there are 5,000 firms in long run equilibrium. What is the short run market supply function?

c. Suppose market demand is  What is the equilibrium price?

What is the equilibrium price?

d. Firms in this industry face a recurring fixed cost FC. What must FC be in order for this industry to indeed be in long run equilibrium with its 100 firms?

What will be an ideal response?

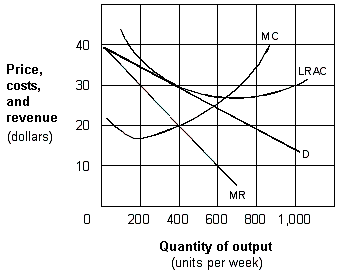

Exhibit 9-3 A monopolistic competitive firm in the long run

?

As presented in Exhibit 9-3, the long-run profit-maximizing output for the monopolistic competitive firm is:

As presented in Exhibit 9-3, the long-run profit-maximizing output for the monopolistic competitive firm is:

A. zero units per week. B. 200 units per week. C. 400 units per week. D. 600 units per week.