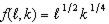

Suppose all firms in a perfectly competitive industry have production processes characterized by the production function  . Suppose the cost of labor is 20 and the cost of capital is 10.

. Suppose the cost of labor is 20 and the cost of capital is 10.

a. Suppose that the industry is in long run equilibrium and that firms are using 1 unit of capital. What is the short run cost function of each firm?

b. Suppose there are 5,000 firms in long run equilibrium. What is the short run market supply function?

c. Suppose market demand is  What is the equilibrium price?

What is the equilibrium price?

d. Firms in this industry face a recurring fixed cost FC. What must FC be in order for this industry to indeed be in long run equilibrium with its 100 firms?

What will be an ideal response?

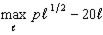

a. The short run production function is  This implies the short run profit maximization problem

This implies the short run profit maximization problem  which solves to

which solves to  Substituting this into the short run production function, we get the short run supply function

Substituting this into the short run production function, we get the short run supply function

b. The SR market supply function is

c. The equilibrium price is found by setting the supply function from (b) equal to the demand function and solving for p. This gives us p*=40.

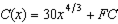

d. For this to be a long run equilibrium, it must be that the lowest point of the long run AC curve happens at an AC of 40. So first we have to calculate the long run AC curve by solving the cost minimization problem to get the conditional input demands

to get the conditional input demands  and

and  . These then give us a cost for the inputs of

. These then give us a cost for the inputs of  . Adding the fixed cost, we have a long run cost function of

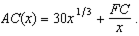

. Adding the fixed cost, we have a long run cost function of  and an average cost function of

and an average cost function of  Taking the derivative of the AC function and setting it to zero, we get that the lowest point of the AC function occurs at

Taking the derivative of the AC function and setting it to zero, we get that the lowest point of the AC function occurs at  . Given our answers to (a) and (b), each firm must be producing 1 unit of output (at a price of 40) -- so we solve

. Given our answers to (a) and (b), each firm must be producing 1 unit of output (at a price of 40) -- so we solve  which gives us FC=10. Plugging that back into the AC curve when x=1, we indeed get AC=40.

which gives us FC=10. Plugging that back into the AC curve when x=1, we indeed get AC=40.

This implies the short run profit maximization problem which solves to Substituting this into the short run production function, we get the short run supply function b. The SR market supply function is

c. The equilibrium price is found by setting the supply function from (b) equal to the demand function and solving for p. This gives us p*=40.

d. For this to be a long run equilibrium, it must be that the lowest point of the long run AC curve happens at an AC of 40. So first we have to calculate the long run AC curve by solving the cost minimization problem

to get the conditional input demands and . These then give us a cost for the inputs of . Adding the fixed cost, we have a long run cost function of and an average cost function of Taking the derivative of the AC function and setting it to zero, we get that the lowest point of the AC function occurs at . Given our answers to (a) and (b), each firm must be producing 1 unit of output (at a price of 40) -- so we solve which gives us FC=10. Plugging that back into the AC curve when x=1, we indeed get AC=40.

Economics

You might also like to view...

In going from the simple to the flexible accelerator, j is set at ________, and v* is ________

A) one, allowed to vary B) one, set at less than one C) less than one, set at less than one D) less than one, set at one E) less than one, allowed to vary

Economics

Explain how the prices of goods and services used in the CPI differ from the prices reflected by GDP deflator

Economics