In long-run equilibrium in perfect competition, every firm is producing at minimum average cost.

Answer the following statement true (T) or false (F)

True

You might also like to view...

If supply is price-inelastic and demand is price-elastic, then the firm can earn positive profits by increasing the price

a. True b. False Indicate whether the statement is true or false

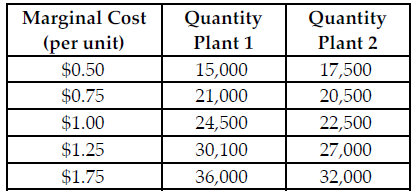

Refer to the table below. If Sweet Grams is a perfectly competitive firm and the market price $1.25 per unit, what is the profit-maximizing quantity for Sweet Grams to produce at Plant 1?

Sweet Grams makes graham cracker snack packages. Sweet Grams is a multi-plant firm with two production facilities. The above table summarizes the total marginal cost of production at various output levels in the separate plants. Assume Sweet Grams is a perfectly competitive firm.

A) 27,000

B) 30,100

C) 36,000

D) 24,500