Once production has reached the maximum average product of labor, if production increases then

A) average fixed cost rises.

B) total costs decrease.

C) total product decreases.

D) decreasing marginal returns occur.

E) the plant size must be increased.

D

Economics

You might also like to view...

In long-run equilibrium under perfect competition,

a. the firm and the industry will have the same cost curves. b. only a very few firms will be earning economic profits. c. the demand curves facing individual firms will fall to the level of minimum AC. d. individual firms will tend to increase their outputs.

Economics

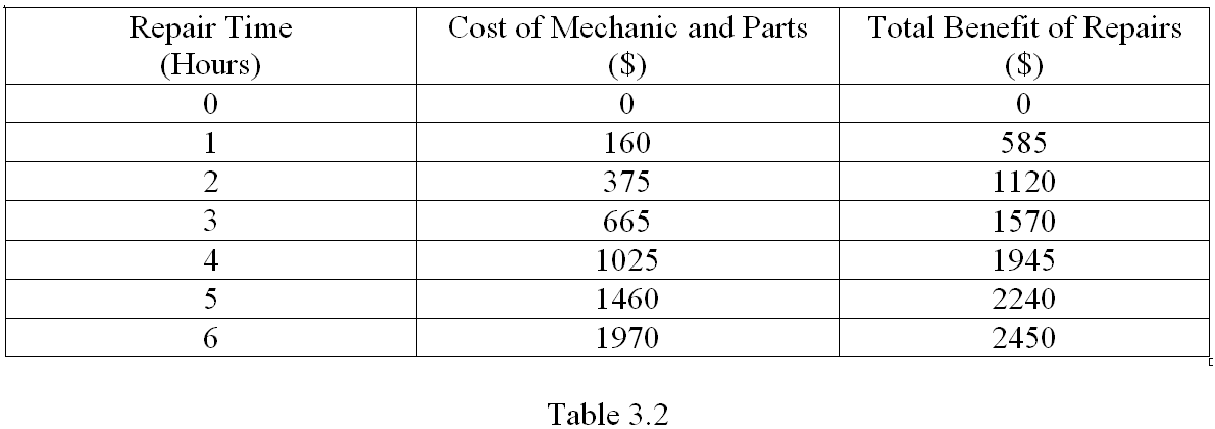

Refer to Table 3.2, which shows some costs and benefits of having your car repaired. Suppose you use your car to deliver pizzas. If you earn $10 per hour delivering pizzas, what is your best choice of hours to spend on car repairs?

A. 2

B. 3

C. 4

D. 5

Economics