Demand in a perfectly competitive market is Q = 100 - P. Supply in that market is Q = P - 10. What is the market equilibrium price and quantity? Given that price and quantity, how much consumer surplus, producer surplus, and deadweight loss is there? If the government imposes a $40 price ceiling, what quantity will be produced and sold? Assuming that those who value the good the most actually get after the ceiling is imposed, how much consumer surplus, producer surplus, and dead-weight loss is there?

What will be an ideal response?

Prior to the tax, the market equilibrium price is $55. The market equilibrium quantity is 45 units. Consumer surplus is 1012.5. Producer surplus is 1012.5. There is no dead-weight loss because the tax has not been imposed yet. After the ceiling is imposed, the quantity supplied is 30 units. Consumer surplus is 450. Producer surplus is 450. Dead-weight loss is now 225.

You might also like to view...

Melanie and Oli are competing Pacific halibut fishers. Both have been allocated ITQs that limit their catch to 1,000 tons of Pacific halibut each. Melanie's cost per ton is $20; Oli's cost per ton is $28. Refer to the information given and assume

that the market price of Pacific halibut is $40 per ton. If Melanie pays Oli $10 per ton for his ITQs and then catches her new limit of 2,000 tons, their combined profit would be: A. $28,000. B. $32,000. C. $30,000. D. $54,000.

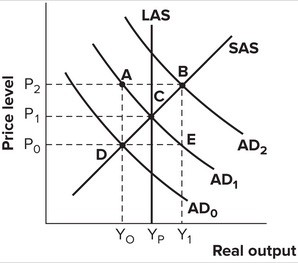

Refer to the graph shown. No changes in fiscal policy are advisable when the economy is at point:

A. A. B. B. C. C. D. D.