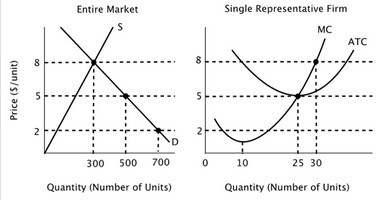

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves. In the long run equilibrium in this market:

In the long run equilibrium in this market:

A. price will equal $5, and there will be 20 firms in the industry.

B. price will equal $5, and there will be 10 firms in the industry.

C. price will equal $5 and total output will equal 500 units, but there is not enough information to determine how many firms will be in the industry.

D. price will equal $8, and there will be 20 firms in the industry.

Answer: A

You might also like to view...

Refer to Figure 5-8. Suppose the emissions reduction target is currently established at 8 million tons. Should society undertake to reduce an additional 1 million tons so that the total reduction is 9 million tons?

A) No, because there is a net cost represented by the area B + C. B) Yes, because toxic fumes are dangerous and must be eliminated at any cost. C) No, because the firms will pass the additional cost on to consumers. D) Yes, because the marginal benefit exceeds the marginal cost at 8 million tons.

What did China create to allow more international trade?

A) Special economic zones B) Foreign exchange centers C) More open and transparent government meetings D) New educational efforts