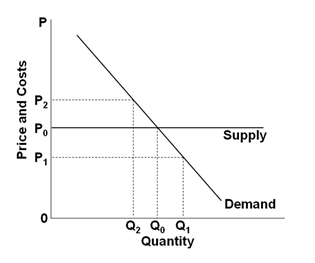

Refer to the graph below, showing the long-run supply and demand curves in a purely competitive market. The curves suggest that this industry is:

A. A constant-cost industry

B. Increasing-cost industry

C. Decreasing-cost industry

D. Not possible, because the supply curve always slopes up

A. A constant-cost industry

You might also like to view...

In the above figure, if the price is $1.25 per gallon of milk and 5 million gallons are produced and consumed, then the consumer surplus is ________ and the producer surplus is ________

A) $3.125 million; $3.125 million B) $12.5 million; $12.5 million C) $6.25 million; $6.25 million D) None of the above answers are correct.

Given that resources can be allocated by the government, the market, a random process, or on a first-come first-serve basis, which of the following statements is true?

a. The market system is not entirely fair but it creates incentives to increase supplies and improve standards of living. b. The random process of allocation allows individuals to acquire purchasing power and enhances the value of the resources that they own. c. Since the government system does not distinguish between those who have income and those that do not, government allocation of resources is the most efficient. d. There will be no shortages under the first-come first-serve basis of allocation. e. A random process of allocation is fair in the sense that everyone gains and there are no losers.