When the production of a good involves several inputs, an increase in the cost of one input will usually cause total costs to

A) rise more than in proportion.

B) rise less than in proportion.

C) remain unchanged.

D) rise by the exact amount of the input price increase.

B

Economics

You might also like to view...

A monopolist would not be able to make a positive profit at any price output combination when

A) marginal cost is less than average total cost for one more unit of output. B) the average variable cost curve is everywhere above the marginal revenue curve. C) the minimum point of the average total cost curve lies to the right of the minimum of the average variable cost curve. D) the average total cost curve is everywhere above the demand curve.

Economics

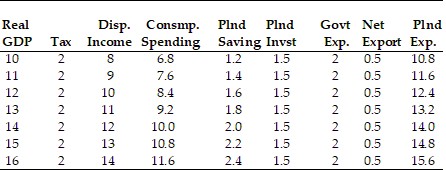

Note: Amounts in billions.Refer to the above table. The equilibrium real GDP is

Note: Amounts in billions.Refer to the above table. The equilibrium real GDP is

A. $14 billion. B. $13 billion. C. $12 billion. D. $15 billion.

Economics