Profit maximization occurs at the quantity where marginal cost equals marginal revenue

a. True

b. False

A

Economics

You might also like to view...

In the long-run, all costs are

a. Fixed costs b. Variable costs c. Sunk Costs d. Marginal Costs

Economics

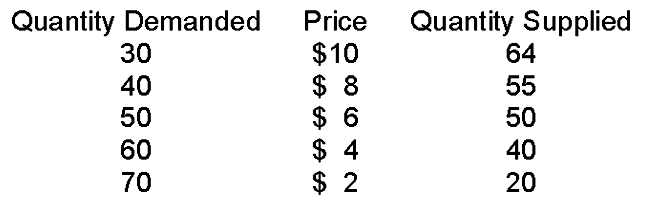

If the government set a price floor at $8

A. there would be a temporary surplus, then prices would fall to equilibrium.

B. there would be a permanent surplus, at least until the price floor was lifted.

C. the price would rise back to the equilibrium price.

D. the price floor would not have any effect on this market.

Economics