In the long run

a. all inputs are fixed.

b. all inputs are variable.

c. some inputs are fixed.

d. production levels never change.

b

Economics

You might also like to view...

Define opportunity cost

Economics

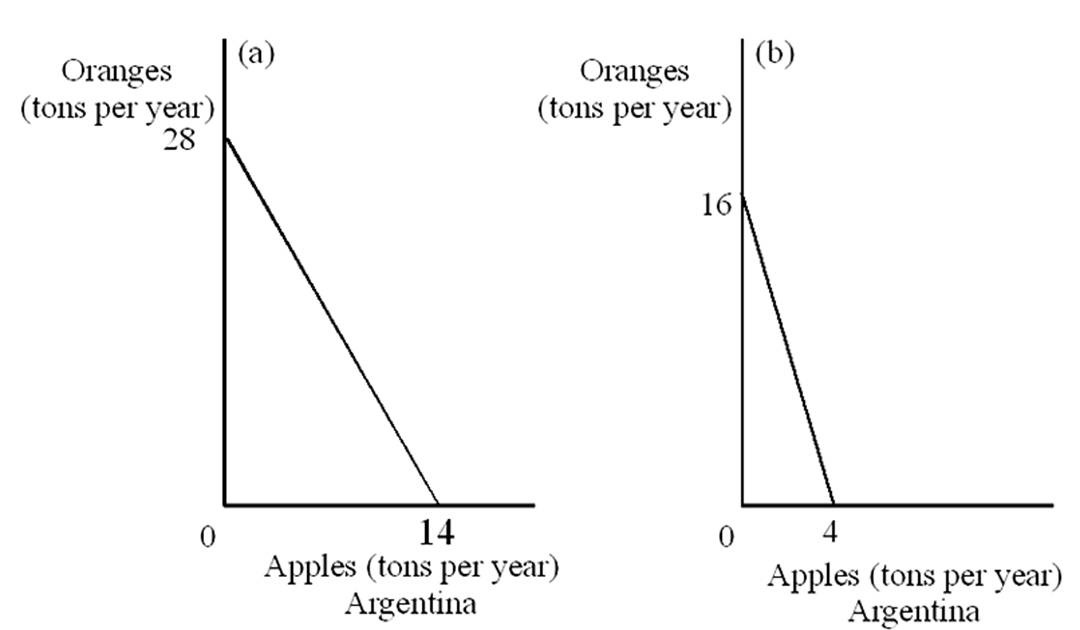

What is the opportunity cost of 1 ton of apples for the nations of Argentina and Brazil, respectively?

A. 4 tons of oranges and 2 tons of oranges

B. 2.5 tons of oranges and .4 tons of oranges

C. .25 tons of oranges and .5 tons of oranges

D. 2 tons of oranges and 4 tons of oranges

Economics