When a monopolistically competitive firm is in a long-run equilibrium, the values of marginal cost, average total cost, and price are all the same

a. True

b. False

Indicate whether the statement is true or false

False

Economics

You might also like to view...

For an individual who has special talent as an entertainer, a large proportion of his salary can be considered

A) a fixed cost. B) economic rent. C) a payment below opportunity cost. D) non-taxable income.

Economics

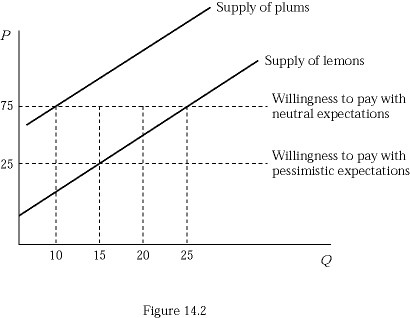

Figure 14.2 represents the market for used cameras. Suppose buyers are willing to pay $125 for a plum (high-quality) used camera and $25 for a lemon (low-quality) used camera. If buyers believe that 50% of used cameras in the market are lemons (low quality), how many plums (high quality) will be supplied by sellers?

Figure 14.2 represents the market for used cameras. Suppose buyers are willing to pay $125 for a plum (high-quality) used camera and $25 for a lemon (low-quality) used camera. If buyers believe that 50% of used cameras in the market are lemons (low quality), how many plums (high quality) will be supplied by sellers?

A. 10 B. 15 C. 20 D. 25

Economics