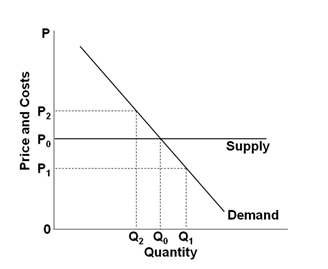

Refer to the graph below, showing the long-run supply and demand curves in a purely competitive market. We know that in this market, the marginal:

A. Cost equals marginal benefit at P1Q1

B. Benefit exceeds marginal cost at the output level of Q2

C. Cost exceeds marginal benefit at the output level of Q2

D. Cost equals marginal benefit at all points on the supply curve

B. Benefit exceeds marginal cost at the output level of Q2

You might also like to view...

The increase in the average unemployment rate in the 1970s was the result of

A) higher real wage rates. B) an increase in the birth rate in the early 1970s. C) repeated increases in the minimum wage. D) an increase in the birth rate in the late 1940s and early 1950s. E) the reduction of overly generous unemployment benefits in the 1970s.

Refer to Table 4-7. If a minimum wage of $12.50 an hour is mandated, what is the quantity of labor demanded?

A) 80,000 B) 550,000 C) 630,000 D) 1,180,000