Answer the following statement(s) true (T) or false (F)

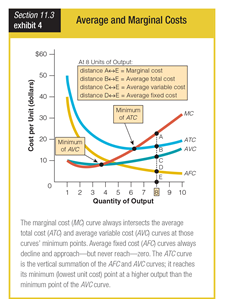

1. In Average and Marginal Costs, the firm will reach peak production when the AFC curve reaches zero.

2. When a firm’s marginal product rises, its marginal cost rises in proportion.

3. When a firm’s marginal product is increasing, its average cost is decreasing.

4. In an appliance factory, the average cost of producing a refrigerator will be relatively high both when very few units are being produced and when production output is especially large.

5. Economists define the long run as anything more than one year in the future.

1. FALSE

2. FALSE

3. TRUE

4. TRUE

5. FALSE

You might also like to view...

When the opportunity cost of producing more of a good is increasing, the marginal cost of producing more of the good is

A) decreasing. B) constant. C) increasing. D) More information is needed to answer the question.

If a market reflects a shortage and prices are allowed to move:

A) supply will increase. B) demand will decrease. C) price will decrease. D) price will increase.