A competitive market is in equilibrium. Then there is a decrease in demand and a decrease in supply. The equilibrium price ________, and the equilibrium quantity ________

A) rises; decreases

B) perhaps changes but we can't say if it rises, falls, or stays the same; decreases

C) falls; increases

D) perhaps changes but we can't say if it rises, falls, or stays the same; increases

E) rises; increases

B

Economics

You might also like to view...

Summarize the historical growth record of the United States over the past 50 years in terms of real GDP growth and in terms of real GDP per capital growth. What three qualifications should be made about these growth rates?

What will be an ideal response?

Economics

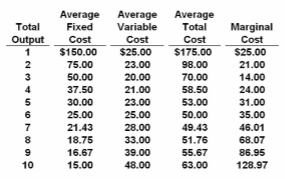

Refer to the data. If the market price for this firm's product is $24, it will produce:

A. 4 units at a loss of $150.

B. 6 units at a loss of $90.

C. 3 units at an economic profit of zero.

D. 4 units at a loss of $138.

Economics