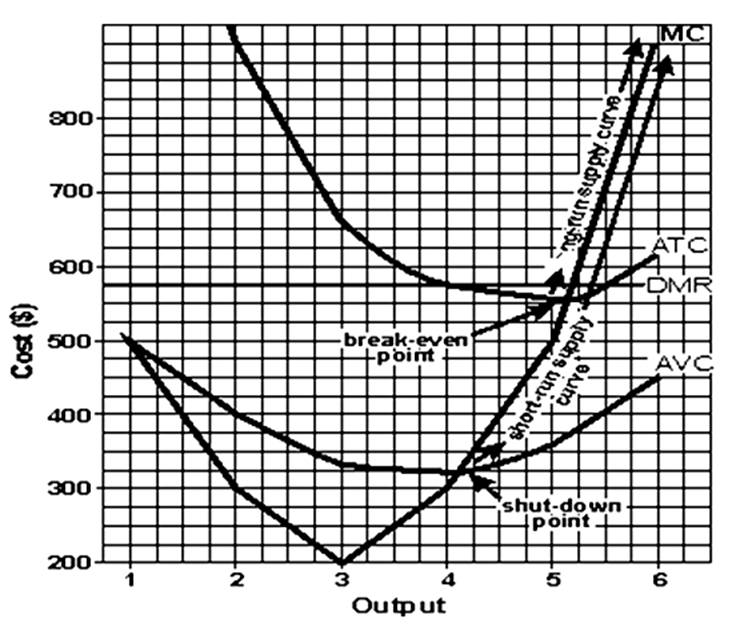

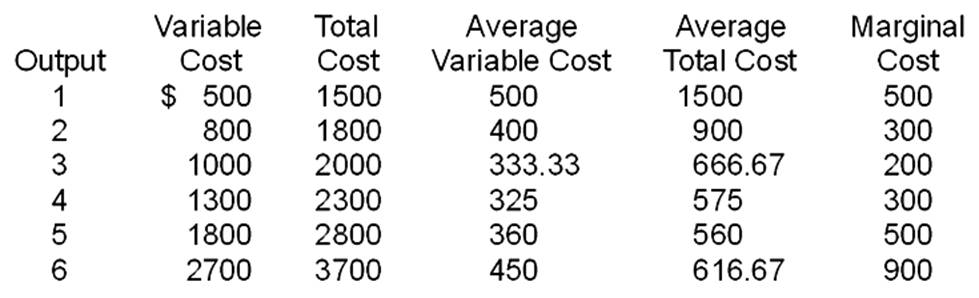

You should do this problem in three steps. First: Fill in Table 1. Assume fixed cost is $1000 and price is $575. Second: Draw a graph of the firm's demand, marginal revenue, average variable cost, average total cost, and marginal cost curves on a piece of graph paper. Be sure to label the graph correctly. On the graph, indicate the break-even and shutdown points and the firm's short-run and long-run supply curves. Third: Calculate total profit in the space below, then answer questions a through d. (a) The minimum price the firm will accept in the short run is $_______. (b) The minimum price the firm will accept in the long run is $_______. (c) The output at which the firm will maximize profits is _______. (d) The output at which the firm will operate most efficiently is ________.

Table 1:

Table 2:

Total profit= (Price - ATC) × output

= ($575 - $560) × 5.2

= $15 × 5.2

= $78 (Must be slightly over $75.)

(a) $324. (b) $558. (c) 5.2. (d) 5.15

Table 2:

You might also like to view...

In the complete algebraic formulation of ISLM,

A) the government spending multiplier is greater than the tax mulitplier as long as b <1. B) the government spending mulitplier is less than the tax multiplier as long as b<1. C) monetary policy is always more powerful than fiscal policy. D) fiscal policy is always more powerful than monetary policy.

If a particular perfectly competitive industry uses only a small fraction of the supply of any of its inputs, the long run supply curve for that industry will tend to be: a. vertical

b. upward sloping. c. horizontal. d. downward sloping.