The marginal cost is the

a. same as the variable cost when output is increasing

b. change in total cost as the quantity changes by one unit

c. change in average variable cost as the quantity changes by one unit

d. change in total fixed cost as the quantity changes by one unit

e. same as the fixed cost when average fixed cost is at a minimum

B

You might also like to view...

If individuals decide to save more for retirement,

A) the supply of loanable funds will shift rightward. B) the supply of loanable funds will shift leftward. C) the demand for loanable funds will shift rightward. D) the demand for loanable funds will shift leftward. E) an excess supply of loanable funds emerges and persists.

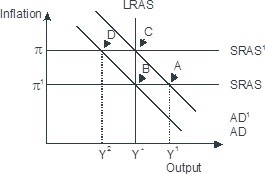

Based on the figure below. Starting from long-run equilibrium at point C, a decrease in government spending that decreases aggregate demand from AD1 to AD will lead to a short-run equilibrium at__ creating _____gap.

A. B; no output B. D; an expansionary C. B; recessionary D. D; a recessionary