Suppose a price-taking firm uses a single input - labor - to produce an output x. The production technology has diminishing marginal product of labor throughout.

a. On a graph with labor hours on the horizontal and output on the vertical axis, illustrate the production frontier for this firm.

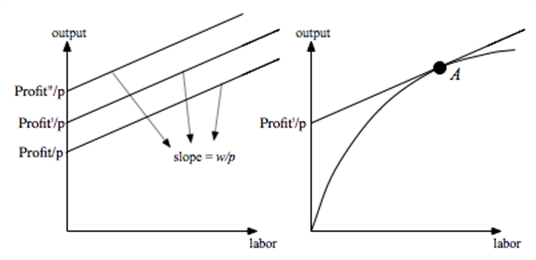

b. For a given wage rate w and output price p, illustrate three isoprofit curves corresponding to profit levels ?

What will be an ideal response?

a.

b. At the profit maximizing production plan A,

c. All production plans that lie on the production frontier are cost-minimizing.

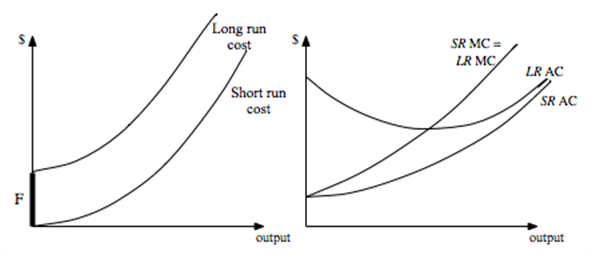

d. e.

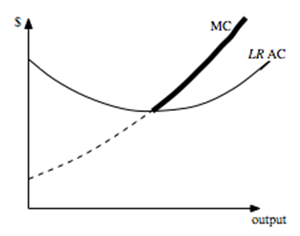

f. The short-run supply curve is the entire MC curve --- including the dashed and solid parts below. The long run supply curve is just the solid part that lies above the long run AC curve.

g. Yes, because the long run equilibrium price is determined by the lowest point of the marginal firm's long run AC curve -- which is the same for firms in both industries.

h. The number went down in industry A and up in industry B -- because the quantity demanded falls more in industry A than in industry B. Firms therefore exit industry A and enter industry B.

b. At the profit maximizing production plan A,

c. All production plans that lie on the production frontier are cost-minimizing.

d. e.

f. The short-run supply curve is the entire MC curve --- including the dashed and solid parts below. The long run supply curve is just the solid part that lies above the long run AC curve.

g. Yes, because the long run equilibrium price is determined by the lowest point of the marginal firm's long run AC curve -- which is the same for firms in both industries.

h. The number went down in industry A and up in industry B -- because the quantity demanded falls more in industry A than in industry B. Firms therefore exit industry A and enter industry B.

Economics

You might also like to view...

People who run their own businesses

A) can keep their labor costs down by not hiring any employees. B) have lower labor costs if they dislike working for anyone else than if they don't mind working for others. C) have no labor costs unless the business is incorporated. D) have the same labor costs as people who hire employees to run their businesses.

Economics

Which of the following firms best fits the definition of a monopoly?

a. General Motors b. Exxon Mobile c. Local electric utility d. AT&T

Economics