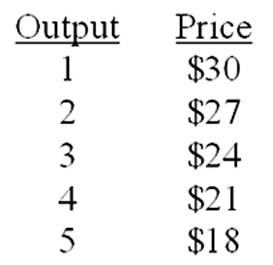

If the marginal cost were $18, output would be

A. 1.

B. 2.

C. 3.

D. 4.

C. 3.

You might also like to view...

In each of the following situations, list what will happen to the equilibrium price and the equilibrium quantity for a particular product, which is a normal good

a. The price of inputs decrease b. The price of a complement increases c. The number of producers in the market increases d. Income increases e. The price of a substitute in production increases

Assume the market price for tangerines is $18.00 per bushel. At the market price, tangerine growers are willing to supply a quantity of 12,000 bushels per week. The quantity supplied drops to zero when the price falls to $5.00 per bushel. Construct a

graph showing this data, calculate the total producer surplus in the market for tangerines, and show the total producer surplus on the graph. Your supply curve should be a straight line. What will be an ideal response?