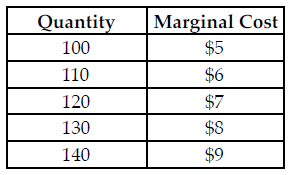

Refer to the table below. The perfectly competitive firm has a random demand with a 50 percent chance of being $7 and a 50 percent chance of being $9. What quantity should the firm produce to maximize its expected profit?

The above table summarizes the marginal cost of production at various quantity levels for a perfectly competitive firm.

A) 130

B) 110

C) 120

D) 140

A) 130

Economics

You might also like to view...

If a firm produces nothing, which of the following costs will be zero?

a. total cost b. fixed cost c. opportunity cost d. variable cost

Economics

Money serves as a medium of exchange. This means that you can

A. increase the economic growth rate in the long run by printing more money. B. compare values across several items by looking at the prices in terms of money. C. accept money as payment for the goods and services you sell. D. hold on to money to use at a later time.

Economics