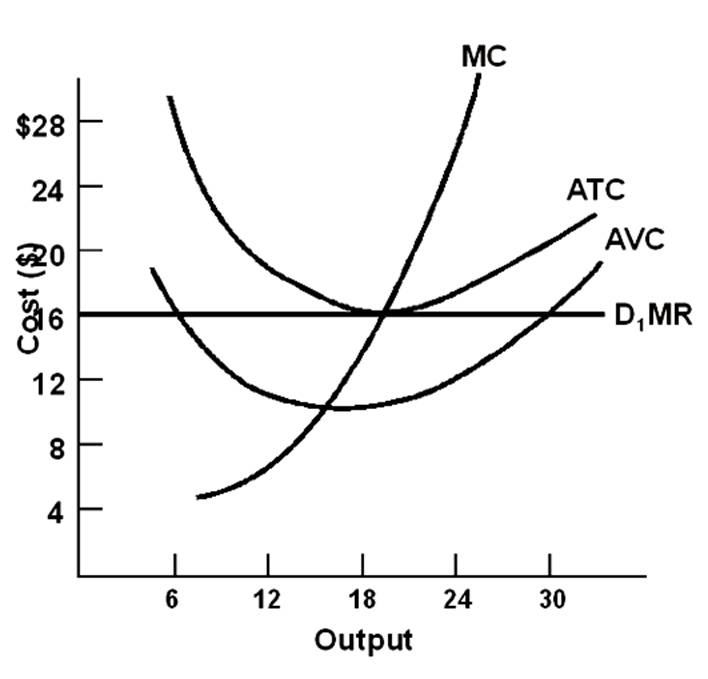

What is the lowest price the firm would accept in the short run?

$10

Economics

You might also like to view...

If demand increases while supply decreases, then the equilibrium price

A) always increases. B) always decreases. C) may increase, decrease, or stay the same. D) never changes.

Economics

The price for used cars is well below the price of new cars of the same general quality. This is an example of:

a. The Degree of Operating Leverage b. A Lemon's Market c. Redeployment Assets d. Cyclical Competition e. The Unemployment Rate

Economics