Describe the relationship between marginal cost and average total cost

What will be an ideal response?

If marginal cost for a given output is below average total cost, average total cost will decrease as output increases but if marginal cost is above average total cost, average total cost will increase as output increases. If marginal cost equals average total cost, average total cost is at its minimum value.

You might also like to view...

The above figure shows the U.S. market for 1 carat diamonds. With free trade, the price in the United States for diamonds is equal to ________ and with the quota illustrated in the figure, the price in the United States is equal to ________

A) $4,000; $2,000 B) $2,000; $3,000 C) $4,000; $3,000 D) $2,000; $2,000 E) $2,000; $4,000

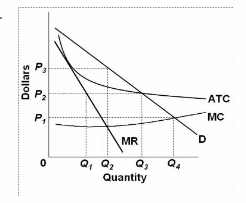

Refer to the diagram for a natural monopolist. If a regulatory commission were to set a maximum price of P 3 , the monopolist would:

A. maximize profits.

B. increase output beyond the profit-maximizing level.

C. reduce output below the profit-maximizing level.

D. be unable to make a normal profit.