Refer to Table 8.3 . Assume the price of labor is $5.00 and the price of capital is $10.00 and the firm's fixed costs are $15

What production technique will be used to produce the first unit of output? The second? The third? What are the firm's total variable costs, total costs, and marginal costs of producing one unit of output? Two units of output? Three units of output?

The firm will produce the first unit using technique B, the second unit using technique A, and be indifferent between techniques A and B for the third unit. TVC are $25, $45, and $60; TC are $40, $60, and $75; MC are $25, $20, and $15

You might also like to view...

The income of consumers increases. and the wage rate in the seafood industry increases. As a result

A) the price of seafood stays the same and the quantity sold can either increase or decrease, depending on whether the change in demand is greater than the change in supply. B) the price of seafood increases and the quantity sold can either increase, decrease or stay the same depending on whether the change in demand was greater than the change in supply. C) the equilibrium quantity sold increases and price can either increase or decrease, depending on whether the change in demand is greater than the change in supply. D) the equilibrium quantity sold can either increase or decrease and the price can either increase or decrease, depending on whether the change in demand was greater than the change in supply.

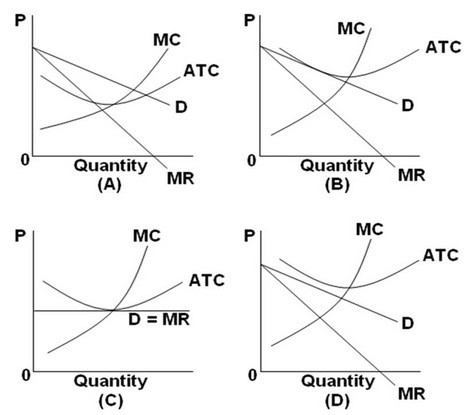

Refer to the above graphs. A short-run equilibrium that would produce losses for a monopolistically competitive firm would be represented by graph:

Refer to the above graphs. A short-run equilibrium that would produce losses for a monopolistically competitive firm would be represented by graph:

A. A. B. B. C. C. D. D.