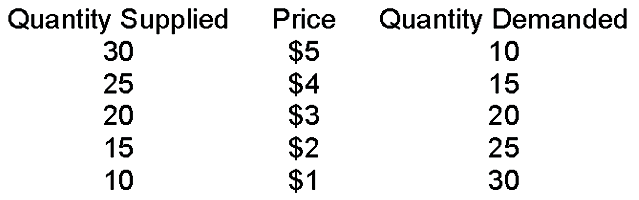

When the price is $5

A. quantity supplied is greater than quantity demanded and, therefore, price must rise to get to equilibrium.

B. quantity supplied is greater than quantity demanded and, therefore, price must fall to get to equilibrium.

C. quantity demanded is greater than quantity supplied and, therefore, price must rise to get to equilibrium.

D. quantity demanded is greater than quantity supplied and, therefore, price must fall to get to equilibrium.

B. quantity supplied is greater than quantity demanded and, therefore, price must fall to get to equilibrium.

You might also like to view...

A cost due to an increase in activity is called

A) an incentive loss. B) a marginal cost. C) a negative marginal benefit. D) the total cost.

As the number of substitutes for a good increases, its own-price elasticity becomes more

a. Unitary b. Relatively elastic c. relatively inelastic. d. perfectly inelastic.