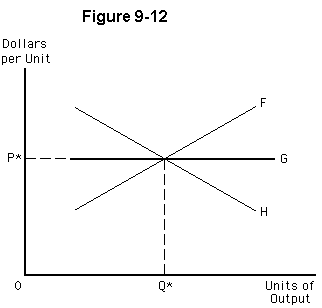

Figure 9-12 shows three possible long-run supply curves for an industry that is currently in equilibrium with price (P*) and quantity (Q*). Which of the following statements is correct?

a.

The long-run supply curve would be F for a decreasing-cost industry, H for an increasing-cost industry, and G for a constant-cost industry.

b.

All three long-run supply curves indicate that the firms' LRATC curves shift as industry output expands.

c.

If the industry uses a significant portion of a scarce input, the long-run supply curve would likely be curve H.

d.

An industry that moves along long-run supply curve F earns above-normal profits in the long run.

e.

If an increase in market output leads to lower prices for a key input, the long-run supply curve would likely be curve H.

e

You might also like to view...

Personal income taxes are reduced as part of an expansionary fiscal policy. What is the impact on aggregate expenditures and income?

A) Both increase. B) Both decrease. C) Aggregate expenditure increases and income decreases. D) Aggregate expenditure decreases and income increases.

Assume Congress decides that oil companies are making too much profit and decides to increase the tax on oil companies for each gallon of gasoline produced. This would

A) guarantee a decrease in profits. B) guarantee an increase in profits. C) guarantee an increase in tax revenues. D) None of the above.