If the price of inputs rises and personal income taxes rise:

a. Aggregate demand rises, and aggregate supply falls.

b. Aggregate demand rises, but aggregate supply does not change.

c. Aggregate demand falls, and aggregate supply rises.

d. Aggregate demand and aggregate supply rise.

e. Aggregate demand and aggregate supply fall.

.E

Economics

You might also like to view...

Firm ownership in the United Kingdom is largest for

A) individuals. B) financial institutions ? agents. C) financial institutions ? ownership/control. D) nonfinancial corporations.

Economics

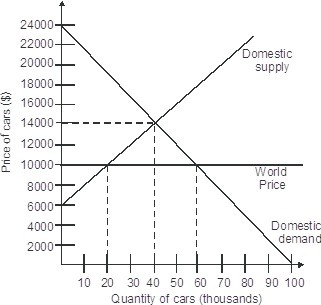

If this is an open economy, the price of a car will be ________.

A. $8,000/car B. $6,000/car C. $10,000/car D. $14,000/car

Economics