When demand for a product increases but the supply of the product remains unchanged, the equilibrium price of the product will

a. rise and equilibrium quantity will decrease.

b. fall.

c. first fall and then return to the original level.

d. rise, and equilibrium quantity will increase.

d. rise, and equilibrium quantity will increase.

Economics

You might also like to view...

Which of the following does a price index typically measure?

a. the change in the money supply b. the change in price of a good or service c. the change in the price of a bundle of goods and services d. the change in relative price of a good or service

Economics

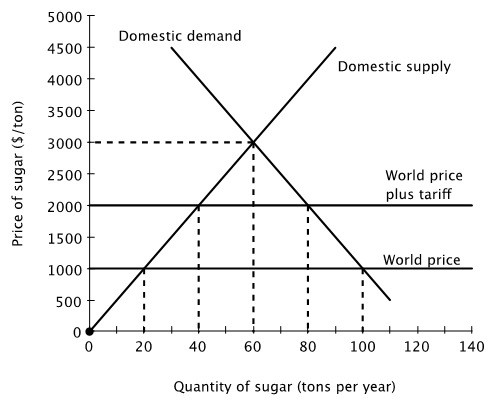

What is the amount of tariff imposed on a ton of sugar?

A. $1,000 B. $500 C. $1 D. $50

Economics