The term opportunity cost refers to

A. The minimum price that a producer will accept for a product.

B. The most a consumer is willing to exchange to get an item.

C. The slope of the demand line for a consumer or slope of the supply line for the producer.

D. All of the choices are correct.

Answer: D

Economics

You might also like to view...

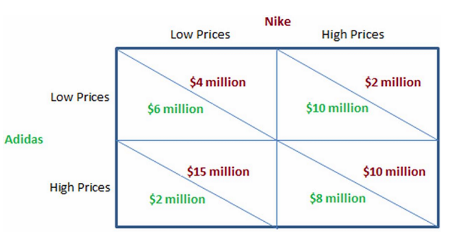

The outcome of the game in the figure show predicts that Nike will earn profits of:

A. $2 million.

B. $4 million.

C. $10 million.

D. $15 million.

Economics

Costs that are "fixed":

A. are those that will never change. B. depend on what timescale you are thinking. C. vary with output, but not with resource prices. D. None of these is true.

Economics