Which of the following occurs when a market is in equilibrium?

A) quantity supplied is equal to quantity demanded

B) supply is equal to demand.

C) the price of the good will tend to rise, all else held constant.

D) the price of the good will tend to fall, all else held constant.

A

Economics

You might also like to view...

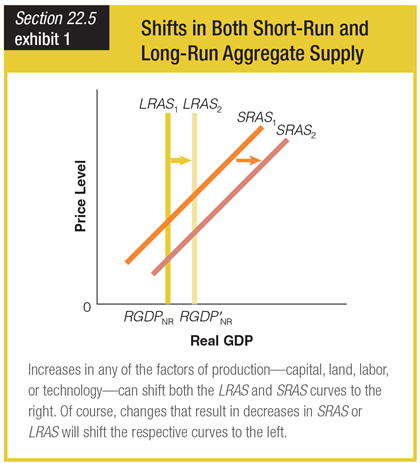

An increase in short-run aggregate supply shifts the curve ______.

a. from SRAS2 to SRAS1

b. from LRAS2 to SRAS1

c. from SRAS1 to LRAS1

d. from SRAS1 to SRAS2

Economics

The classical economic doctrine held that the normal equilibrium position of the economy was one of

a. rising interest rates. b. some unemployment. c. rising prices. d. full employment.

Economics