Total cost is the

a. amount a firm receives for the sale of its output.

b. fixed cost less variable cost.

c. market value of the inputs a firm uses in production.

d. quantity of output minus the quantity of inputs used to make a good.

c

Economics

You might also like to view...

A rent control is an example of a ________

A) price floor B) price ceiling C) negative externality D) positive externality

Economics

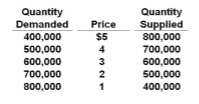

Refer to the table. For each of the 100 firms in this industry, marginal revenue and total revenue will be:

A. $4 and $400, respectively.

B. $3 and $30,000, respectively.

C. $4 and $20,000, respectively.

D. $3 and $18,000, respectively.

Economics